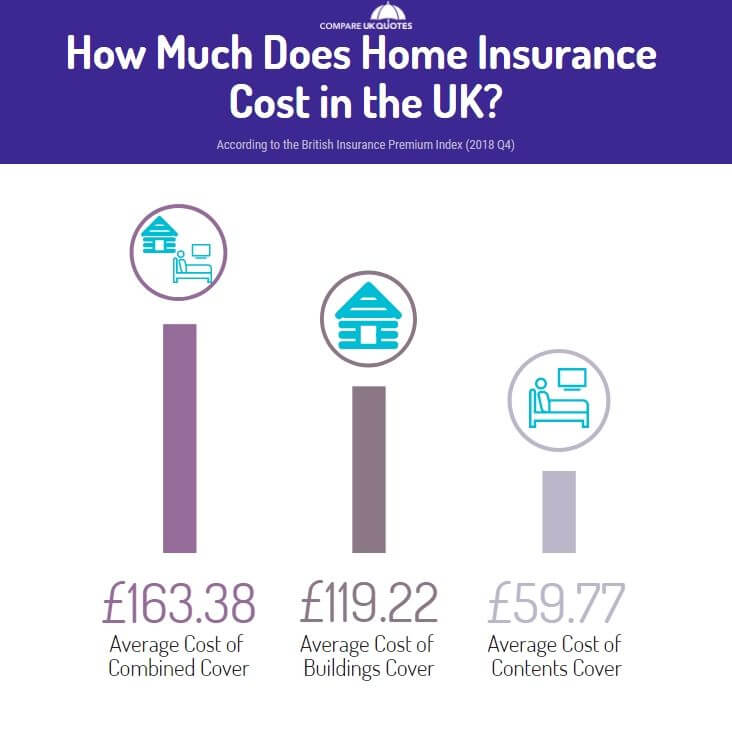

Inspect your contract language thoroughly to see what perils are specifically covered (or not covered), as well as what your insurance coverage will pay to change or repair. House insurance coverage usually offers a level of liability protection. If somebody falls and injures themselves in your driveway, for example, the policy can pay if you were to be taken legal action against. Like the majority of type of insurance coverage, the cost will differ. Elements that identify your overall cost for premiums consist of just how much your home is worth, any outdoors structures, how you utilize your residential or commercial property and the overall value of your belongings. The final expense can be hundreds as much as countless dollars hilton timeshare yearly, depending on how low you desire your deductible and whether you cover the full replacement expense of the home and its contents.

You desire a policy that suffices to change the structure and contents of your home if it's ruined or damaged. Policyholders expect to have temporary accommodations while a new living plan is being prepared. A leading policy will include exceptional customer support and make the claims process easy. The expense of home insurance coverage is really personalized and follows a formula based on a variety of aspects. What might be the least expensive company in one area might not be as inexpensive in another part of the nation. Your house type, such as single-family versus condo, might modify the rates, also.

To get the best price on a policy, search with numerous business. There are numerous methods to keep property owners insurance costs down. Here are a couple of typical methods: Raise your deductible to secure a lower rate. Pay your premiums upfront, rather of through regular monthly payments. Package with your auto or life insurance coverage. Enhance your credit. Make enhancements to the security and security of your home, such as consisting of extra fire prevention or house security innovation. (Not all policies will lower sell my timeshare now your rate for these enhancements, however.) Going several years without filing a claim can have a long-term, favorable impact on your rates.

Determining how much insurance coverage you need starts with calculating the replacement value of your house, or a comparable home http://daltongzxy058.yousher.com/get-this-report-on-what-is-epo-insurance if it had to be rebuilt today. Then, include the expense to replace your belongings, including any valuables or items that may not be quickly acquired. Lastly, consider the expense of an average liability claimit might be much higher than the $100,000 limit in most fundamental policies. Speak with your insurance coverage agent or business to see how these elements can be integrated into a detailed house policy that protects your interests. A few of the top house insurer in the U.S., according to Bankrate, are: Amica Mutual Allstate Metlife Geico Farmers Standard house insurance doesn't generally cover flooding, either from natural occasions or from structural failure.

Like other policies, flood insurance coverage does not cover pre-existing water damage or a flood that's currently in development at the time the client buys the policy. Tenants insurance is a group of protections bundled into one policy that can protect tenants from unforeseen damage or loss. It covers their home, their usage of the residential or commercial property and liability that others may look for against them. Here are Bankrate's picks for the best occupants insurance provider. While the policy rate will vary by client and kind of residential or commercial property covered, renters insurance is budget-friendly. Typical monthly premiums variety from $15 to $30 a month.

How Much Does Car Insurance Cost Things To Know Before You Get This

Renters insurance likewise provides some liability protection, safeguarding you versus claims if someone is harmed in your leased house. An excellent tenants insurance coverage policy will likewise secure other individuals's home from damage the taken place in your house, in addition to the cost for you to live elsewhere while your home is brought back after an occasion.

Insurance coverage is something most individuals don't even want to believe about up until they require it the a lot of. However, comprehending what is and isn't covered in your property owners insurance policy can indicate the difference of being able to rebuild your house and replace your individual belongings. Property owners require to do annual insurance coverage "check ups" to make certain they keep up with local building expenses, house renovation and inventories of their individual belongings. The typical house owners insurance coverage covers damage arising from fire, windstorm, hail, water damage (omitting flooding), riots and surge as well as other reasons for loss, such as theft and the extra cost of living elsewhere which the structure is being repaired or reconstructed.

Click on this link for more details on general liability coverage and umbrella policies. The Structure of Your House Replacement Cost. Insurance that pays the policyholder the expense of changing the harmed home without deduction for depreciation, however limited to an optimal dollar quantity. Extended Replacement Cost. An extended replacement cost policy, one that covers costs approximately a certain portion over the limitation (generally 20%). This provides you defense against such things as an abrupt increase in building expenses. Actual Cash Worth. This covers the cost to change your house minus devaluation costs for age and use. For instance, if the life span of your roofing system is twenty years and your roof is 15 years old, the cost to replace it in today's marketplace is going to be much higher than its actual cash worth.

That's not the market value, however the cost to restore. If you do not have enough insurance coverage, your company may just pay a portion of the expense of replacing or fixing harmed items. Here are some ideas to help make sure you have enough insurance: For a fast estimate on the amount to reconstruct your home: increase the local building costs per square foot by the total square video footage of your home. To discover out the structure rates in your area, consult your regional contractors association or a trustworthy home builder. You ought to likewise consult your insurance coverage agent or company agent.

Aspects that will determine the cost to reconstruct your home: a) building costs b) square video footage of the structure c) type of exterior wall constructionframe, masonry or veneer d) the style of the home (ranch, colonial) e) the variety of rooms & restrooms f) the type of roofing system g) attached garages, fireplaces, outside trim and other unique features like arched windows or special interior trim. Inspect the value of your insurance coverage against rising regional structure expense EACH YEAR. Consult your insurance coverage agent or company representative if they offer an "INFLATION GUARD CLAUSE. When is open enrollment for health insurance." This immediately changes the home limitation when you restore your policy to reflect present building expenses in your area.

How How Much Auto Insurance Do I Need can Save You Time, Stress, and Money.

Examine the current building codes in your community. Building regulations require structures to be built to minimum standards. If your home is badly damaged, you may have to restore it to comply with the new standards requiring a change in design or structure products. These usually cost more. Do not guarantee your home for the market value. The expense of reconstructing your home might be greater or lower than the cost you paid for it or the rate you could sell it for today. Many lenders need you to purchase adequate insurance to cover the quantity of your mortgage. Make sure it's likewise enough to cover the cost of restoring.